Category Archives: Market Insights

Nickel Digital Team Reenforced By Another Senior Goldman Alumnus Hire

Nickel Digital Asset Management (Nickel), Europe’s largest regulated and award-winning digital assets hedge fund manager, founded by senior traders and investment professionals from major wall street banks, has announced the hiring of Henry Howell, a Goldman alumnus with eighteen years of experience in hedge fund, derivatives, and electronic futures sales. Henry is joining Nickel as Head of Business Development.

Prior to joining Nickel, Henry Howell was with Eisler Capital, a London-based macro hedge fund. Before that, Henry spent sixteen years with Goldman Sachs in Chicago and London. As a Managing Director in the Prime Services business unit in London, Henry was the head of listed and OTC derivatives sales and the global head of electronic futures.

Launched in early 2019, Nickel Digital offers institutional-grade access to digital assets market and currently runs four crypto funds catering for various degree of investors’ risk tolerance, from market-neutral arbitrage to multi manager and liquid venture strategies. Nickel has seen its assets under management increase over 300% in the past 12 months, with AUM now approaching the $200 million mark. Its flagship Digital Assets Arbitrage Fund delivered 24 months of all-positive performance since inception, with solid double digits returns YTD and Sharpe ratio of 4.8.

Anatoly Crachilov, co-Founder and CEO of Nickel Digital, commented:

“We are absolutely delighted to welcome Henry to our actively growing team. From three founding partners 2 years ago, Nickel has now expanded into a team of 25 and I am specifically pleased to see a growing number of Wall Street professionals embracing the digital assets space, and another Goldman alumnus reinforcing Team Nickel. Henry brings an impressive 16 years of experience in top positions at Goldman, which will be invaluable to our ambitious roll out of investment offerings across the world.”

Henry Howell commented:

“As a specialised crypto asset manager, Nickel Digital are uniquely positioned in the rapidly evolving digital space. Nickel’s expertise, track record of risk management and dedicated infrastructure all combine to make it a trusted partner for institutional investors. I am hugely excited to be joining the talented team at Nickel Digital and helping to expand the business globally going forward.”

Nickel Digital’s infrastructure is designed to offer various access points to the crypto market:

Nickel currently has four funds investing in the digital asset space. Its market-neutral Digital Asset Arbitrage Fund pursues an absolute return strategy without expressing directional views on the underlying cryptoassets market. It exploits market inefficiencies and price dislocations and harnesses swings of volatility to deliver consistent positive returns within a strictly defined risk management framework. Since inception 24 months ago, the fund has delivered strong risk-adjusted returns with no drawdown months and a Sharpe ratio above 4.

Nickel Diversified Alpha (Digital Factors) Fund is a non-directional, multi-strategy fund which wraps a portfolio of attractive, hard-to-access and capacity-constrained strategies into a single, investible fund. Among the strategies it deploys are high-frequency market making, statistical arbitrage, relative value, volatility arbitrage and momentum.

Nickel Digital Leaders DeFi Fund is designed to capture the growth potential of the broader digital assets space by identifying the emerging technologies in Decentralised Finance, digital asset trading and decentralised applications.

Nickel’s Digital Gold Institutional Fund, a Bitcoin tracker, provides secure, efficient, transparent, and liquid access to physically allocated Bitcoin. It delivers institutional-grade precision of trade execution available on both weekdays and weekends with one of the industry’s lowest expense ratios.

Finally, a new Defensive Bitcoin Fund is expected to be launched soon to cater to clients seeking partial downside protection to their bitcoin position, while still capturing the upside offered by the structural expansion of the digital assets space.

Bitcoin Is Winning the Covid-19 Monetary Revolution

The virtual currency is scarce, sovereign and a great place for the rich to store their wealth.

In “Shuggie Bain,” Douglas Stuart’s award-winning and harrowing depiction of alcoholism, sectarianism and deprivation in post-industrial Scotland, money is always scarce and often dirty. Deserted by her second husband and unable to hold down a job, Shuggie’s mother, Agnes, relies on her twice-a-week child benefit to feed her children — or her booze habit. As the latter nearly always wins, she and Shuggie are regularly reduced to desperate expedients to fend off starvation: Extracting coins from electricity and television meters, pawning their few valuable possessions, and ultimately selling their bodies for brutal sexual favors.

Stuart vividly captures the miseries of a Glasgow of greasy coins and filthy banknotes. After one of many wretched copulations in the back of a taxi, one of Agnes’s lovers inadvertently showers her with coins from his pocket. Shuggie’s father briefly reappears at one point, handing his son two 20-pence pieces from his taxi’s change dispenser by way of a gift, grudgingly adding four 50-pence pieces when the boy looks nonplused. (“Don’t ask for mair!”) The “rag-and-bone man,” who goes from house to house buying old clothes and junk, pays “with a roll of grubby pound notes” bound by an old Band-Aid. The image is especially startling because banknotes have so rarely featured in the narrative. The only credit in this world is from rent-to-own catalogues, the Provident doorstep lender, and a few hard-pressed shopkeepers.

I grew up in middle-class, mostly sober Glasgow, but I still remember the tyranny of those damned coins: the nightmare of having too few for a bus fare or the wrong sort for a phone box. To my children, all this is as much a part of ancient lore as pirate chests of doubloons once were to me. Coins are fast fading from their lives, soon to be followed by banknotes. In some parts of the world — not only China but also Sweden — nearly all payments are now electronic. In the U.S., debit card transactions have exceeded cash transactions since 2017. Even in Latin America and parts of Africa, cash is yielding to cards and a growing number of people manage their money through their phones.

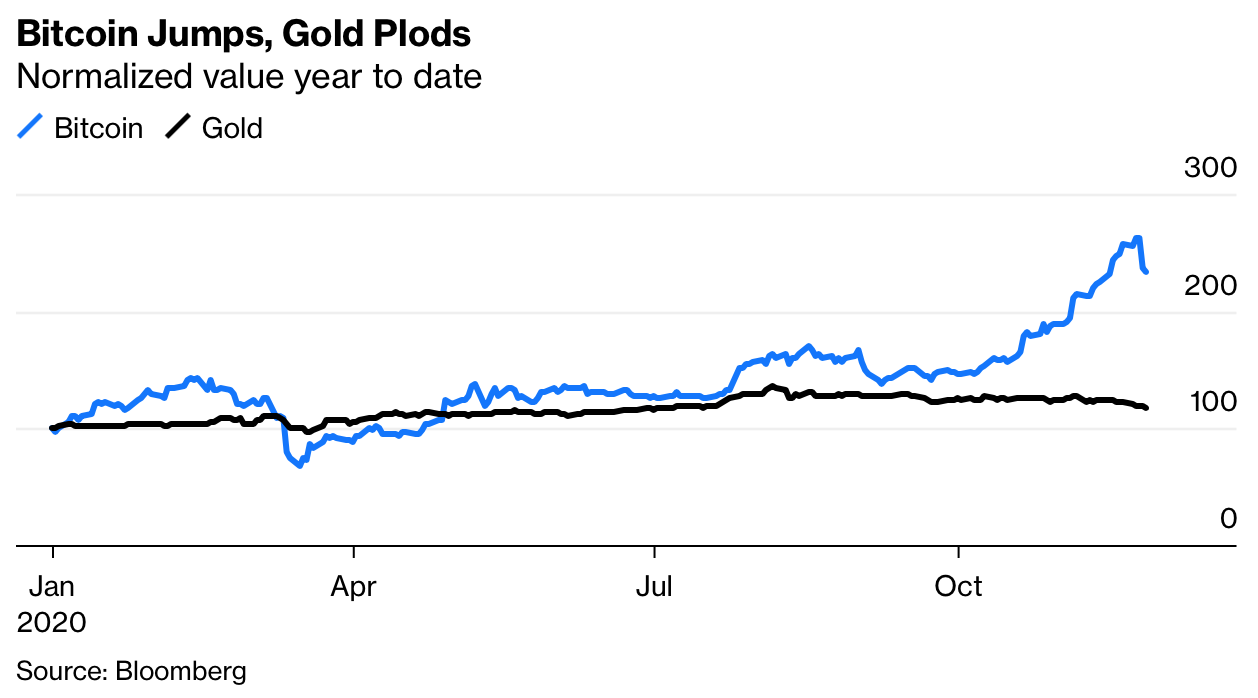

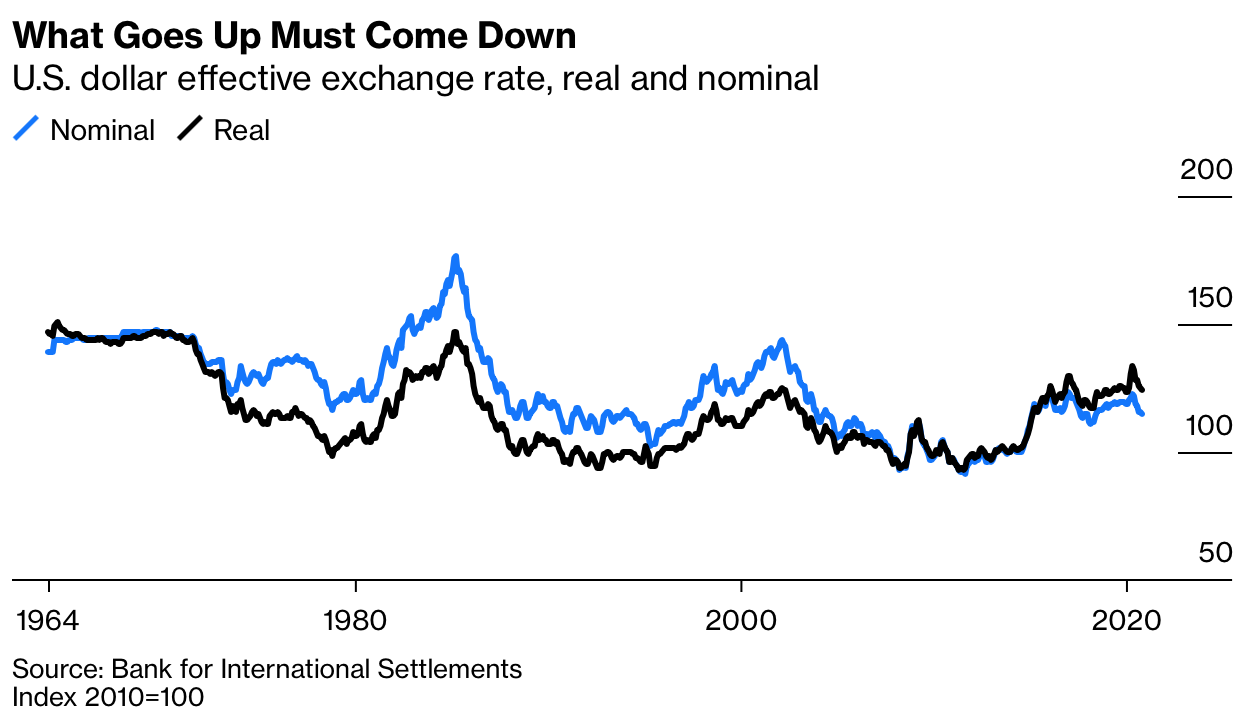

We are living through a monetary revolution so multifaceted that few of us comprehend its full extent. The technological transformation of the internet is driving this revolution. The pandemic of 2020 has accelerated it. To illustrate the extent of our confusion, consider the divergent performance of three forms of money this year: the U.S. dollar, gold and Bitcoin.

The dollar is the world’s favorite money, not only dominant in central bank reserves but in international transactions. It is a fiat currency, its supply determined by the Federal Reserve and U.S. banks. We can compute its value relative to the goods consumers buy, according to which measure it has scarcely depreciated this year (inflation is running at 1.2%), or relative to other fiat currencies. On the latter basis, according to Bloomberg’s dollar spot index, it is down 4% since Jan. 1. Gold, by contrast, is up 15% in dollar terms. But the dollar price of a bitcoin has risen 139% year-to-date.

This year’s Bitcoin rally has caught many smart people by surprise. Last week’s high was just below the peak of the last rally ($19,892 according to the exchange Coinbase) in December 2017. When Bitcoin subsequently sold off, the New York University economist Nouriel Roubini didn’t hold back. Bitcoin, he told CNBC in February 2018, had been the “biggest bubble in human history.” Its price would now “crash to zero.” Eight months later, Roubini returned to the fray in congressional testimony, denouncing Bitcoin as the “mother of all scams.” In tweets, he referred to it as “Shitcoin.”

Fast forward to November 2020, and Roubini has been forced to change his tune. Bitcoin, he conceded in an interview with Yahoo Finance, was “maybe a partial store of value, because … it cannot be so easily debased because there is at least an algorithm that decides how much the supply of bitcoin raises over time.” If I were as fond of hyperbole as he is, I would call this the biggest conversion since St. Paul.

Roubini is not the only one who has been forced to reassess Bitcoin this year. Among the big-name investors who have turned bullish are Paul Tudor Jones, Stan Druckenmiller and Bill Miller. Even Ray Dalio admitted the other day that he “might be missing something” about Bitcoin.

Financial journalists, too, are capitulating: On Tuesday, the Financial Times’s Izabella Kaminska, a long-time cryptocurrency skeptic, conceded that Bitcoin had a valid use-case as a hedge against a dystopian future “in which the world slips towards authoritarianism and civil liberties cannot be taken for granted.” She is on to something there, as we shall see.

So what is going on?

First, we should not be surprised that a pandemic has quickened the pace of monetary evolution. In the wake of the Black Death, as the historian Mark Bailey noted in his masterful 2019 Oxford Ford lectures, there was an increased monetization of the English economy. Prior to the ravages of bubonic plague, the feudal system had bound peasants to the land and required them to pay rent in kind, handing over a share of all produce to their lord. With chronic labor shortages came a shift toward fixed, yearly tenant rents paid in cash. In Italy, too, the economy after the 1340s became more monetized: It was no accident that the most powerful Italian family of the 15th and 16th centuries were the Medici, who made their fortune as Florentine moneychangers.

In a similar way, Covid-19 has been good for Bitcoin and for cryptocurrency generally. First, the pandemic accelerated our advance into a more digital word: What might have taken 10 years has been achieved in 10 months. People who had never before risked an online transaction were forced to try, for the simple reason that banks were closed. Second, and as a result, the pandemic significantly increased our exposure to financial surveillance as well as financial fraud. Both these trends have been good for Bitcoin.

I never subscribed to the thesis that Bitcoin would go to zero after it plunged in price in late 2017 and 2018. In the updated 2018 edition of my book, “The Ascent of Money” — the first edition of which appeared more or less simultaneously with the foundational Bitcoin paper by the pseudonymous Satoshi Nakamoto — I argued that Bitcoin had established itself as “a new store of value and investment asset — a type of ‘digital gold’ that provides investors with guaranteed scarcity and high mobility, as well as low correlation with other asset classes.”

“Satoshi’s goal,” I argued, “was not to create a new money but rather to create the ultimate safe asset, capable of protecting wealth from confiscation in jurisdictions with poor investor protection as well as from the near-universal scourge of currency depreciation … Bitcoin is portable, liquid, anonymous and scarce … A simple thought experiment would imply that $6,000 is therefore a cheap price for this new store of value.”

Two years ago, I estimated that around 17 million bitcoins had been mined. The number of millionaires in the world, according to Credit Suisse, was then 36 million, with total wealth of $128.7 trillion. “If millionaires collectively decided to hold just 1% of their wealth as Bitcoin,” I argued, “the price would be above $75,000 — higher, if adjustment is made for all the bitcoins that have been lost or hoarded. Even if the millionaires held just 0.2% of their assets as Bitcoin, the price would be around $15,000.” We passed $15,000 on Nov. 8.

What is happening is that Bitcoin is gradually being adopted not so much as means of payment but as a store of value. Not only high-net-worth individuals but also tech companies are investing. In July, Michael Saylor, the billionaire founder of MicroStrategy, directed his company to hold part of its cash reserves in alternative assets. By September, MicroStrategy’s corporate treasury had purchased bitcoins worth $425 million. Square, the San Francisco-based payments company, bought bitcoins worth $50 million last month. PayPal just announced that American users can buy, hold and sell bitcoins in their PayPal wallets.

This process of adoption has much further to run. In the words of Wences Casares, the Argentine-born tech investor who is one of Bitcoin’s most ardent advocates, “After 10 years of working well without interruption, with close to 100 million holders, adding more than 1 million new holders per month and moving more than $1 billion per day worldwide,” it has a 50% chance of hitting a price of $1 million per bitcoin in five to seven years’ time.

Whoever he is or was, Satoshi summed up how Bitcoin works: It is “a purely peer-to-peer version of electronic cash” that allows “online payments to be sent directly from one party to another without going through a financial institution.” In essence, Bitcoin is a public ledger shared by a network of computers. To pay with bitcoins, you send a signed message transferring ownership to a receiver’s public key. Transactions are grouped together and added to the ledger in blocks, and every node in the network has an entire copy of this blockchain at all times. A node can add a block to the chain (and receive a bitcoin reward) only by solving a cryptographic puzzle chosen by the Bitcoin protocol, which consumes processing power.

Nodes that have solved the cryptographic puzzle — “miners,” in Bitspeak — are rewarded not only with transaction fees (5 bitcoins per day, on average), but also with additional bitcoins — 900 new bitcoins per day. This reward will get cut in half every four years until the total number of bitcoins reaches 21 million, after which no new bitcoins will be created.

There are three obvious defects to Bitcoin. As a means of payment, it is slow. The Bitcoin blockchain can process only around 3,000 transactions every 10 minutes. Transaction costs are not trivial: Coinbase will charge a 1.49% commission if you want to buy one bitcoin.

There is also a significant negative externality: Bitcoin’s “proof-of-work” consensus algorithm requires specialized computer chips that consume a great deal of energy — 60 terawatt-hours of electricity a year, just under half the annual electricity consumption of Argentina. Aside from the environmental costs, one unforeseen consequence has been the increasing concentration of Bitcoin mining in a relatively few hands — many of them Chinese — wherever there is cheap energy.

But these disadvantages are outweighed by two unique features. First, as we have seen, Bitcoin offers built-in scarcity in a virtual world characterized by boundless abundance. Second, Bitcoin is sovereign. In the words of Casares, “No one can change a transaction in the Bitcoin blockchain and no one can keep the Bitcoin blockchain from accepting new transactions.” Bitcoin users can pay without going through intermediaries such as banks. They can transact without needing governments to enforce settlement.

The advantages of scarcity are obvious at a time when the supply of fiat money is exploding. Take M2, a measure of money that includes cash, bank accounts (including savings deposits) and money market mutual funds. Since May, U.S. M2 has been growing at a year-on-year rate above 20%, compared with an average of 5.9% since 1982. The future weakness of the dollar has been a favorite 2020 talking point for Wall Street economists such as Steve Roach. You can see why. There really are a lot of dollars around, even if their velocity of circulation has slumped because of the pandemic.

The advantages of sovereignty are less obvious but may be more important. Bitcoin is not the only form of digital money that has flourished in 2020. China has been advancing rapidly in two different ways.

Nowhere in the world are mobile payments happening on as large a scale as in China, thanks to the spectacular growth of Alipay and WeChat Pay. Those electronic payment platforms now handle close to $40 trillion of transactions a year, more than double the volume of Visa and Mastercard combined, according to calculations by Ribbit Capital. The Chinese platforms are expanding rapidly abroad, partly through investments in local fintech companies by Ant Group and Tencent.

At the same time, the People’s Bank of China has accelerated the rollout of its digital currency. The potential for a digital yuan to be adopted for remittance payments or cross-border trade settlements is substantial, especially if — as seems likely — countries participating in the One Belt One Road program are encouraged to use it. Even governments that are resisting Chinese financial penetration, such as India, are essentially building their own versions of China’s electronic payments systems.

Some economists, such as my friend Ken Rogoff, welcome the demise of cash because it will make the management of monetary policy easier and organized crime harder. But it will be a fundamentally different world when all our payments are recorded, centrally stored, and scrutinized by artificial intelligence — regardless of whether it is Amazon’s Jeff Bezos or China’s Xi Jinping who can access our data.

In its early years, Bitcoin suffered reputational damage because it was adopted by criminals and used for illicit transactions. Such nefarious activity has not gone away, as a recent Justice Department report makes clear. Increasingly, however, Bitcoin has an appeal to respectable individuals and institutions who would like at least some part of their economic lives to be sheltered from the gaze of Big Brother.

It is not (as the term “cryptocurrency” misleadingly implies) that Bitcoin is beyond the reach of the law or the taxman. When the Federal Bureau of Investigation busted the online illegal goods market Silk Road in 2013, it showed how readily government agencies can trace the counterparties in suspect Bitcoin transactions. This is precisely because the blockchain is an indelible record of all Bitcoin transactions, complete with senders’ and receivers’ bitcoin addresses.

Moreover, the Internal Revenue Service is perfectly prepared to demand information on bitcoin accounts from exchanges, as Coinbase discovered in 2016. A rumor of new U.S. Treasury regulations requiring greater disclosures by exchanges caused a sharp crypto selloff over Thanksgiving. The point is simply that the financial data of law-abiding individuals is better protected by Bitcoin than by Alipay. As the Stanford political theorist Stephen Krasner pointed out more than 20 years ago, sovereignty is a relative concept.

Rather than seeking to create a Chinese-style digital dollar, Joe Biden’s nascent administration should recognize the benefits of integrating Bitcoin into the U.S. financial system — which, after all, was originally designed to be less centralized and more respectful of individual privacy than the systems of less-free societies.

Life in the East End of Glasgow in the 1980s was nasty, brutish and short of money. But all those transactions in grubby pounds and pence — genuine shitcoins — were, if nothing else, private. If Agnes Bain bought Special Brew instead of oven chips, it was a matter for her, the shopkeeper, and her long-suffering kids; the state was none the wiser. That was scant consolation to poor Shuggie. But, as we have learned again this year, a free society comes at a price that is not always payable in cash.

Is Bitcoin a Viable Hedge Against the Great Monetary Inflation?

The Bank of England is seeking a third-party supplier to develop a mobile wallet for a central bank digital currency (CBDC).

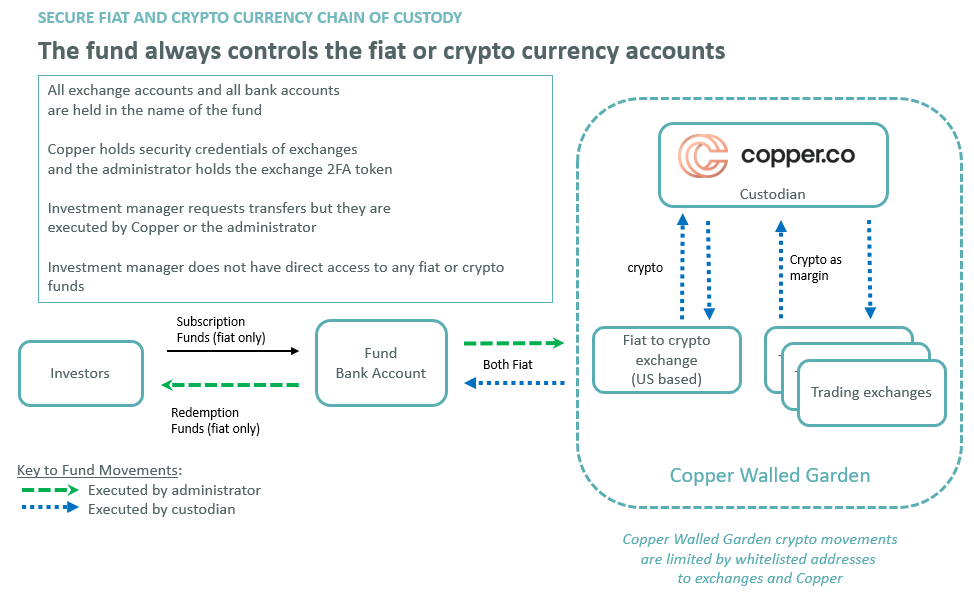

Independent custody for crypto hedge funds trading on multiple exchanges

Problem: Self-custody for crypto hedge funds

We believe that self-custody for crypto hedge funds trading on multiple exchanges is not a viable institutional solution (see this article on self-custody we wrote earlier). In short, although many custodians claim to have institutional custody, in practice they lose control of the fund’s crypto assets as soon as they are sent to an exchange.

At Nickel Asset Management, we have been seeking to set up a crypto arbitrage fund for some time, but we decided to launch only once a solution to self-custody was available. To achieve this, we have been working with the London-based custodian, Copper, who have developed a working solution to the self-custody problem.

Solution: The Walled Garden

This solution creates a wall that surrounds the fund’s custodian and the exchanges on which the fund trades. Inside the Walled Garden, crypto transfers can be made frequently, rapidly and safely. Moving crypto funds outside the Walled Garden, if ever needed, requires signatures of multiple independent parties for maximum safety.

The diagram below illustrates the key points of the Walled Garden solution:

1. All the fund’s transfer requests pass through the custodian, and the custodian instructs the exchanges on receipt of a transfer request.

2. The investment manager does not have access to the exchanges for transfers, while continuing to have access to the exchanges for trading.

3. A fund transfer outside of the Walled Garden requires cooperation between the custodian and the administrator. No one entity is entitled to make such a transfer.

The Walled Garden

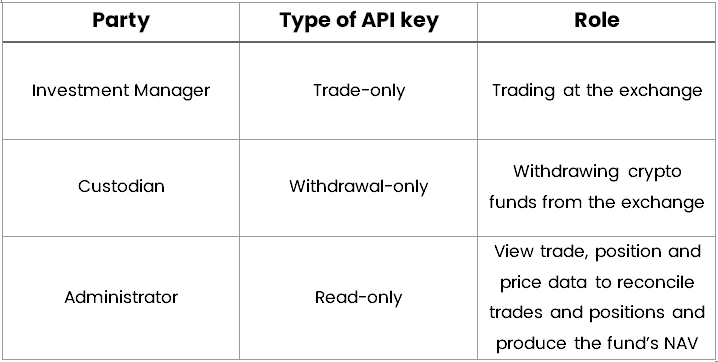

In order for any exchange to operate within the Walled Garden effectively, it must provide the following functions[1]:

– permissioned API keys (for withdrawals only, for trading only and for reading only)

– a REST API for withdrawals

– a whitelist of addresses for withdrawals

Permissioned API keys enable the various parties of investment manager, custodian and fund administrator to perform their roles:

The REST API for withdrawals enables the custodian to create an automated front-end solution for investment manager to request transfers (e.g. via the custodian’s website). These can then be automatically initiated via an API request to the exchange.

Whitelisted addresses for exchange fund withdrawals ensure that, once they have been set up and the exchange security credentials have been secured, withdrawals from exchanges are restricted to blockchain addresses within the Walled Garden. The only blockchain addresses that will be whitelisted are the fund’s blockchain address (controlled by the custodian) and the exchanges’ blockchain addresses for the fund’s accounts.

How do we add an exchange to the Walled Garden?

The Walled Garden doesn’t appear out of nowhere and it needs to be established. This is our current setup, process which will no doubt be improved upon as exchanges and service providers mature:

1) The investment manager gathers the fund’s KYC documents necessary to open an exchange account and (with fund directors, if necessary) opens the exchange accounts.

2) The investment manager sets up the whitelisted blockchain addresses for the custodian’s account for each crypto used as margin on the exchange (in our case BTC and some stable coins).

3) The investment manager generates the trade-only and read-only API keys for the exchange. The read-only key is given to the administrator.

4) The investment manager passes the exchange security credentials (username and password) to the custodian. No 2FA has been set up as this will be set up by the custodian.

5) The custodian checks whether the whitelisted blockchain addresses set up by the investment manager are the valid addresses of the fund and the fund’s account addresses at other exchanges. The custodian then adds the fund’s new exchange account addresses to its own whitelist.

6) The custodian generates the exchange transfer API key and incorporates it into their system for exchange-to-custody and exchange-to-exchange transfers.

7) The custodian changes the exchange account’s security credentials (email and password) and adds 2FA to the account. This process is actually slightly more involved than this, although for security purposes we do not disclose it fully.

8) The custodian securely stores exchange security credentials and passes an encrypted copy to the administrator to store in case of corruption of the custodian’s systems.

9) The custodian passes the 2FA device to the administrator.

Note that, by this stage:

– logging in to the exchange requires cooperation between the custodian (who has sole access to email and password) and the administrator (who has sole access to 2FA)

– the fund manager no longer has access to the account’s security credentials

– no crypto funds have yet been transferred to the exchange

10) The investment manager can now ask the custodian to send crypto assets to the exchanges for trading and margin. These transfers can only be sent to verified exchange addresses that have previously been whitelisted by the custodian.

Note that, in this setup, crypto withdrawals from the exchange to the custodian or directly to other exchanges (i.e. staying inside the Walled Garden) can be made by the investment manager using the custodian’s system, allowing for efficient cross-exchange trading.

Crypto withdrawals to any other address (i.e. going outside the Walled Garden) are prevented by the exchange’s and custodian’s whitelists and would require an approval from both the custodian and the administrator.

Fiat withdrawals from the Walled Garden are made by the custodian at the request of the fund manager, and only to the fund bank account, operated by the administrator.

What are the drawbacks?

As is often the case, the security of the Walled Garden brings some minor drawbacks in usability, as follows:

Direct access to exchanges

Unless the exchange support sub-accounts, the investment manager does not have direct trading access to the exchange. In order to trade, they have to use the exchange API with a trading bot or an EMS such as Coinigy or Caspian (we will soon publish a review of crypto EMSs). In practice, most managers will use an EMS so they can use more sophisticated orders than those currently offered by the exchanges (e.g. Iceberg).

Changes to exchange account

Occasionally, the investment manager may need to make necessary changes to the exchange account. If the changes are simple, the administrator and the custodian working together can make the changes without providing the investment manager with security credentials.

If the changes are complex, the custodian and administrator can remove the 2FA and reset the exchange security credentials so the manager can assess the account to make the changes. Before this takes place, the manager ought to send all the crypto on the exchange account back to custody. In this way, the manager would only be accessing an empty account.

Summary

The Walled Garden solution, with Copper as custodian, now exists for crypto hedge funds trading on multiple exchanges. This creates a secure area for the fund’s custodian and the exchanges on which it trades. Within the Walled Garden, transfers can be made frequently, rapidly and safely between custody and the intra-mural exchanges. Individually, neither the investment manager, custodian nor administrator could be forced by a criminal party to transfer the fund’s crypto assets from the exchanges.

Institutional investors in hedge funds operating this solution can now be confident that the funds they invest in crypto hedge funds are not self-custodied when held on exchange.

To learn more about the solution contact Copper at hello@copper.co

To learn more about crypto arbitrage contact ir@nickel.am

Written by Michael Hall and Alek Kloda December 2018

[1] Some exchanges also allow main account and sub-accounts making exchange operations simpler. Exchange sub-accounts enable the investment manager to log on to the exchange to trade without having to use an Execution Management System (EMS). This is a feature that only a few exchanges currently offer, although, as the space institutionalizes, it should become widespread. In practice, most investment managers will use an EMS or trading bots to improve market access and reduce slippage.

The Crypto Hedge Fund Self-Custody Problem

A short note on why on exchange crypto assets are insecure

Cryptocurrency fund custodians

A cryptocurrency custodian is a specialized financial institution responsible for safeguarding a firm’s or individual’s cryptocurrency assets. If a firm is only going to hold and not trade crypto assets then it doesn’t need a very sophisticated custody solution. However hedge funds that plan on trading crypto assets on multiple exchanges, require a different and more sophisticated custody solution.

The current hedge fund custody situation

The current trend amongst crypto hedge funds is to appoint a custodian and self-custody the crypto assets that are sent to exchanges.

The self-custody arises because the investment managers of the hedge funds open the exchange accounts on which the fund is going to trade, which means the investment managers have access to the exchange account security credentials. When cryptocurrency is transferred to the exchange for trading or margin, it goes out of control of the custodian and the investment manager is effectively self-custodying the funds.

The problem with self custody

There are three main problems with self-custody

First, it won’t pass the operational due diligence of sophisticated capital allocators whom the crypto industry needs to invest, support and validate the sector. Self-custody is a shirking of a manager’s fiduciary responsibility to its clients.

Secondly it puts the investors at risk of having their assets stolen by a dishonest investment manager. A manager who controls exchange credentials can just add their blockchain address to an exchange account and send themselves the AUM. Think of Madoff, self-custody is like self-administration except the manager can steal all the AUM sent to the exchanges.

Thirdly it puts the manager at risk of murder, violent home invasion and extortion by criminals trying to steal the fund’s crypto assets. There have been enough instances of this to cause self-custodying hedge fund managers sleepless nights. A manager of any fund trading crypto assets should be able to tell a would be attacker that there is no way to transfer the crypto outside the boundaries of a fund. It can only do this if it has an independent custodian that is at all times in control of the crypto assets.

Exchanges : The weak link in institutional custody

Currently many custodians are calling themselves “institutional” custodians. However there are many flavors of institutional custody: If all an institution wants is to go long crypto, then there are many custodians in the USA and Switzerland that will shard keys and store them securely. But if an institution wants to trade on various exchanges or invest in a fund that does, then the fund needs to move crypto assets to an exchange so locking the fund’s private keys away is not possible.

The vulnerability of the funds on the exchange stems from the custodian’s lack of control of the funds on the exchange. No custodians currently set up exchange accounts on behalf of hedge funds. This is currently done by the investment managers which means they then control the exchange security credentials. The exchange credentials can be used to make money transfers from the exchange without the custodian’s knowledge or approval.

Even if the manager were to set up for multi signature approvals for crypto movements (assuming the exchanges support this) the manager controls the account and so can remove the signatures later.

Prime Brokerage for crypto

Although the crypto world is different from the fiat one, there are many parallels between the fiat and the crypto world so when looking at crypto issues it often helps to think of the fiat solution. In the fiat world, hedge funds who trade on exchanges don’t have to open accounts on all the exchanges on which they want to trade. Usually they will appoint a prime broker (PB) or a futures clearer who will open exchange accounts on their behalf. The KYC/AML is done once by the PB and the exchanges either use this KYC or trust in the PB.

The problem with crypto brokers is that they add expense and introduce another level of intermediation.

What is currently missing from “institutional” custody solutions?

1) Exchange credentials should be held by the custodian.

2) Transfers from exchange to fund should be made by the custodian.

In order to control the safety of the assets held by a fund the custodian should be responsible for their movement both to and from exchanges. To do this the custodian should control the exchange credentials and move money from the exchanges back to the fund’s secure storage.

The exchange credentials (log on info, any 2FA) are important as they give access to the exchange account where security measures, such as whitelisted addresses, are setup and can be used to generate API keys to make crypto transfers. The exchange credentials are set up when the fund’s account is opened on the exchange.

Possible solutions to self-custody

A. The crypto custodian broker hybrid

One currently available solution is the crypto-custodian-broker hybrid which resembles a fiat prime broker (i.e. MS or Goldman). In this case the crypto hybrid implements a safe custody solution and opens accounts in its name on several exchanges. When funds want to trade they call the crypto hybrid. The crypto is always under the control of the hybrid.

The disadvantages of this model are that:

1) It’s expensive with some hybrids charging a 1% of volume fee and an additional 50bps custody fee;

2) The fund is limited to trading on the exchanges on which the hybrid has accounts;

3) The hybrids won’t let the managers use their API keys to trade, which rules out certain strategies and will hurt slippage (unless the hybrids have written sophisticated trading algorithms).

This solution doesn’t protect the fund from exchange hacks or exchanges socializing losses as the hybrid will pass on any losses to the fund. This approach means that institutional investor will be paying higher fees and trading with less flexibility than retail investors so it is unlikely to gain wide acceptance. Since when did wholesalers pay more than retail?

B. Digital Asset Receipts

The safest and simplest solution is a Digital Asset Receipt (DAR) AKA token on token. In this solution the fund sends fiat or crypto to the custodian who safely stores it. When the manager wants to trade on an exchange the custodian sends a DAR instead of crypto to the exchange.

The DAR is essentially and IOU that says that the fund is good for the crypto amount and the custodian has reserved it (meaning the manager can’t move it anywhere). When the manager want to take funds off the exchange the DAR custodian checks that that’s OK with the exchange and changes the amount of the DAR on the exchange. If the exchange is hacked, all the hacker will find is an IOU that the custodian can refuse to honor. The DAR is a token on a private blockchain. Inter exchange transfers can also be made very quickly. This approach also simplifies the running of exchanges as they no longer have to custody crypto so reducing the hacking risk. The only problem with this solution is that it isn’t here yet. Koine (koinefinance.com) are currently implementing this and expect to have several major exchanges signed up in Q1 2019.

C. Account opening by trusted third parties

In theory a trusted third party employed by the fund such as a director, administrator, auditor or custodian could open the exchange accounts. After all administrators often open fiat bank accounts for funds, why not exchange accounts?

Unfortunately most of these third parties are unwilling to go through the process of opening accounts in the name of the fund. A few years ago opening exchange accounts only required an email address, now the exchanges ask for extensive KYC and AML documentation.

An additional complication is that the exchange security credentials need to be kept as safe as crypto private keys as access to the exchange account enables moving funds.

Conclusion

Until a reasonably priced, safe end-to-end custody solution exists, self-custody is not viable for institutions investing in hedge funds.

There are currently no truly independent institutional custody solutions for hedge funds that trade on exchanges.

Although Nickel wouldn’t implement this solution itself , it is actively searching for and encouraging it.